Mortgage Rates Stay Low

.

MORTGAGE RATES STAY LOW

On January 30, 2019, the Federal Open Market Committee of the Federal Reserve System “FOMC” had its first monetary policy meeting of 2019. The committee voted to leave the Federal Funds Target Rate (“FFTR”), the rate that banks charge each other for overnight lending, at 2.25% – 2.50%. The Federal Funds Target Rate is a benchmark rate and is used to calculate the United States (Fed) Prime Rate. The United States (Fed) Prime rate is calculated by adding the FFTR + 3%. As of January 30, 2019, the United States Prime Rate is 5.50%.

Determining Your Interest Rate

Banks utilize the target range, the “FFTR,” for the federal funds rate as a starting point to establish the interest rates they want to charge for loans. Banks also use other factors to set their interest rates. The bottom line is that banks want to maximize profits, through the Net Interest Margin. The Net Interest Margin is simply a ratio that measures how successful the bank is investmenting funds compared to the expenses on those investments. Banks want to show shareholders gains, not losses. However, banks also realize consumers and businesses seek the lowest rate possible

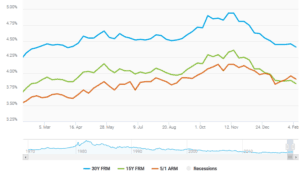

It’s no secret banks adjust interest rates based on risk and the lower the risk, the better the interest rate for a borrower. When borrowers have a high credit score, put up collateral or a large down payment, and use services from the same bank (checking, savings, brokerage, mortgage) they may get a discount on the interest rate. Another strategy may be for a borrower to borrow during a down economy or when uncertainty is high, such as inflation or a volatile interest rate environment, in order to get a favorable rate. So, under these circumstances, a bank may be especially motivated to make a deal or give you the best rate possible. Borrowers who seek out a loan or rate with government backing can also secure the lowest rate possible. The U.S. weekly averages as of February 7, 2019, as reported by Mortgage buyer Freddie Mac, are: 30-Year Fixed Rate Mortgage, 4.41%, 15-Year Fixed Rate Mortgage, 3.84%; 5/1-Year Adjustable Rate Mortgage, 3.91%. This is a 10-month low; however, the current rates are still above last year’s rates by .09%; 30-year Fixed Rate Mortgage rate averaged 4.32%, compared to the current 4.41% rate for a 30-year Fixed Rate Mortgage rate.

Chart of interest rates 2018 to 2019- Freddie Mac

The Outlook

The decision by the FOMC to not increase the Federal Funds Target Rate means banks will keep their interest rates steady as well. This means the Spring of 2019 will be a great time for borrowers to secure mortgages from lenders at historic low interest rates before interest rates increase in the coming months or year.

The next meeting for the FOMC is March 20, 2019 and economic projections will be heard at this meeting. The FOMC meets at least 8 times per year and have a published schedule for the remainder of 2019. It should be noted that the FOMC has indicated plans to raise the rate to 3.6% by 2020 and 3.8% by 2021. This means that by 2020, the United States Prime Rate could be 6.5%, or possibly higher, and lenders will increase mortgage interest rates lock-in-step with the increases by the FOMC. The FOMC meets at least 8 times per year and have a published schedule.

Historically speaking, the FOMC of the Federal Reserve System kept the Federal Funds Target Rate (“FFTR”), the rate that banks charge each other for short-term loans, at zero between 2008 and 2015. The recession ended in June 2009. The Federal Reserve raised the target level of the federal funds rate in 2018 on the following dates by the following percentages:

| Date | FFTR | U.S. (Fed) Prime Rate (+3%) |

| Mar 22, 2018 | 1.75% | 4.75% |

| Jun 14, 2018 | 2.00% | 5.00% |

| Sep 27, 2018 | 2.25% | 5.25% |

| Dec 19, 2018 | 2.50% | 5.50% |

The Federal Funds Target Rate History from 1990 to present is available to view by clicking here.

Recent Comments