2021 Residential Pool Safety Law

Florida Senator Ed Hooper (R) filed residential pool safety bill (SB 124).

Residential pool safety is critical to prevent children from drowning in a pool. In an effort to prevent tragedies from occuring in the future, Florida Senator Ed Hooper (R) filed Florida Senate 2021 Bill (SB 124) [PDF, HTML] on December 4, 2020 for the purpose of amending Florida’s existing residential swimming pool safety law. The new elements or regulations of the bill (SB 124) impact the property owner, as well as, Florida real estate brokers, real estate sales associates, and home inspectors.

Background

The world changed for Brittany Howard on September 28, 2017. On that day, her two-year old son, Kacen Howard, apparently pushed a sliding glass door open and bypassed a pool fence at her home. Brittany Howard’s son, Kacen Howard, ended up drowning in the pool.

The bill (SB 124) was inspired by the drowning death of Kacen Howard and is named the Kacen’s Cause Act. Senators from both sides of the isle have pledged their support for the bill (SB 124). However, a similar bill died in committee during the 2020 session.

The Centers for Disease Control and Prevention data shows an average of 3,536 people drown each year in the United States – about ten deaths per day. The CDC also reports drowning kills more kids ages 1-4, apart from birth defects, and is the second-leading cause of unintentional injury-related death behind motor vehicle crashes involving children.

Current Residential Pool Safety Law In Florida

Florida Chapter 515; Residential Swimming Pool Safety Act, regulates safety feature options at homes and provides for penalties when not in compliance with the law. Under current law, only one of Florida’s listed safety measures is required to be implemented around a pool. Do not confuse the “safety feature options” with “pool barrier requirements.”

Consequences for non-compliance with swimming pool regulations

A property owner, who is also typically the homeowner, that fails to implement a pool safety feature as required by Chapter 515 Florida Statutes commits a misdemeanor of the second degree. Under current law, this could send the property owner to jail for up to 60 days and/or fined $500. Fortunately, the law also provides a waiver of penalties if compliance with the law occurs within 45 days of being arrested, issued a summons, or the issuance of a Notice To Appear (NTA).

Florida’s residential swimming pool safety feature options as listed in F.S.S. 515.27:

- The pool at a home must be isolated from access to a home by an enclosure that meets the pool barrier requirements of s. 515.29 – (4 feet high, no gaps, no openings, placed around pool perimeter, etc.);

- The pool at a home must be equipped with an approved safety pool cover;

- All doors and windows providing direct access from the home to the pool must be equipped with an exit alarm that has a minimum sound pressure rating of 85 dB A at 10 feet;

- All doors providing direct access from the home to the pool must be equipped with a self-closing, self-latching device with a release mechanism placed no lower than 54 inches above the floor; or

- A swimming pool alarm that, when placed in a pool, sounds an alarm upon detection of an accidental or unauthorized entrance into the water. Such pool alarm must meet and be independently certified to ASTM Standard F2208, titled “Standard Safety Specification for Residential Pool Alarms,” which includes surface motion, pressure, sonar, laser, and infrared alarms. For purposes of this paragraph, the term “swimming pool alarm” does not include any swimming protection alarm device designed for individual use, such as an alarm attached to a child that sounds when the child exceeds a certain distance or becomes submerged in water.

Florida’s Residential Pool Safety Law Overhaul

Florida Senate 2021 Bill (SB 124) [PDF, HTML] has amendments attempting to prevent serious injury or death at the home along with significant additions to the existing law language aimed at preventing a child of a new homeowner from inheriting a potential death trap. The new legislative language impacts property owners, licensed home inspectors, and licensed real estate brokers and their sales associates.

Pick at least two regulations

The amendment provides a list of approved pool safety feature options. A property owner must pick at least two to satisfy the proposed language of the bill (SB 124).

- “(1) In order to pass final inspection and receive a certificate of completion, a residential swimming pool must meet at least two one of the following requirements relating to pool safety features:”

But, there’s a catch to the two requirement rule that sounded somewhat palatable.

Amendments to residential pool safety feature options – tacked on

It’s not just pick two pool safety feature options, instead of one, and move on in 2021.

In addition to the requirement of implementing two of the pool safety feature options, the pool safety feature options have amendments to themselves as well. While it may seem innocuous now, it could become difficult in the future for a property owner and, in turn, for a potential buyer of the property.

For example, the first option, which refers to a pool being isolated by a barrier, has the following added to the end of the existing sentence, “and ASTM Standard F2286, titled “Standard Design and Performance Specification for Removable Mesh Fencing for Swimming Pools, Hot Tubs, and Spas.” ASTM is an acronym for American Society for Testing and Materials. The ASTM standard was last updated January 1, 2016 from its previous version in 2005. So, when ASTM decides to update their standard, legislators do not have to contemplate amending the statute again as the ASTM Standard F2286 is incorporated in the legislation.

A problem could arise should additional, cost-prohibitive standards, become the norm in a later revision, i.e. requirements to install an enhanced design of a non-climbable fence. Rather than list the additional language, it would be more prudent for the reader to view them on the Florida Senate website for Senate Bill 124 (SB 124) starting at line 33 of the bill text.

Compliance required to sell a parcel

There are two additional requirements in the bill (SB 124) that directly impacts a property owner wanting to sell their home. One of the additional requirements is placed in Paragraph (2) of Section 515.27, Florida Statutes, regulating pool design, and the other additional requirement comes in the form of adding Paragraph (d) to subsection (1) of Section 468.8323, Florida Statutes, which regulates home inspections.

- A residential pool must have at least two of the pool safety feature options. The bill (SB 124) states, “A property owner may not transfer, for consideration, ownership of a parcel that includes a swimming pool unless the swimming pool meets at least two of the requirements under subsection (1).”

- Prior to the sale of a home with a pool, a licensed home inspector must furnish a certified report disclosing the pool and any safety devices. The bill (SB 124) states, ” (1) The home inspector shall report: …. (d) If there is a swimming pool, as defined in s. 515.25, any safety features, as described in s. 515.27(1), which are present.”

Yes, this has implications for property owners who want to sell “For Sale By Owner,” for property owners who use a licensed real estate broker or sales associate, and for licensed home inspectors. This proposed amendment delivers new provisions that most may initially overlook.

Drilling down finds potential problems

A comparison of the ASTM Standard from 2005 with the current standard from January 1, 2016 could not be done. Unfortunately, the publication with the standards is not public domain and must be purchased on the ASTM International website for about $42. Several government organizations published brochures incorporating the ASTM F2286 guidelines, from prior years, in their material for pool design and performance.

Ironically, a publication discussing ASTM Standard F2286, was published by the Consumer Product Safety Commission, entitled Safety Barrier Guidelines for Residential Pools. The Consumer Product Safety Commission’s guide appears to be a 2012 version, with a footnote of “Publication 362 (08/12).” Now, the Florida Department of Health appears to have a newer version of Safety Barrier Guidelines for Residential Pools with a footnote of “Publication 362 (04/15)” The PoolSafely.gov website, referred to in these government publications, also has the “Publication 362 (08/12)” in the footer and is published to their website. I was unable to find any publicly available reference to the ASTM F2286 standards that went into effect on January 1, 2016.

Comparing Guides Using ASTM Standards

There is additional content in the guide from the Florida Department of Health compared to the guide from the Consumer Product Safety Commission. A single page excerpt is below and shows the new content. It is unknown if the additional content is derived from the January 2016 version of ASTM F2286 Standards or if the additional content is merely suggestions made by the Florida Department of Health.

The fact that standards, by which government entities rely upon for enforcement, are not publicly accessible from ASTM and freely available is a concern. This is because a property owner should be able to refer to the guidelines so that they can ensure compliance. Theoretically, a contractor installing a pool, safety barriers, and covers should know the requirements but that is not always the case. Ultimately, it is the property owner’s liability.

The proposed language in the bill (SB 124) only refers to “ASTM Standard F2286” and not to a year in which the standards were published for reference. A court could make the determination the law is ambiguous. The same goes for pool coverings as the proposed language in the bill (SB 124) only refers to “ASTM Standard F1346.” Even ASTM International refers to the 2005 version of ASTM F2286 as “F 2286 – 05” incorporating the year of the standards with the designation.

Inconsistent Legislative Intent

Now, perhaps failing to include a year in the ASTM Standards was an oversight. Maybe that is so, but it would not explain why the amendment to paragraph (e) of Section 515.27, Florida Statutes regarding swimming pool alarms clearly restricts and clearly states what year of the standard will apply. Legislators intentionally included the year for Underwriters Laboratories, Inc. (UL) standards, to wit: “. . . [a]nd must comply with the Underwriters Laboratories, Inc., ‘Standard for General-Purpose Signaling Devices and Systems,’ UL 2017.”

Exploiting An Oversight

Who would benefit from such an oversight or seek to exploit it? It is not hard to believe that those in the pool and leisure industries could network with, or already have ties to, ASTM staff to create additional standards. Why do such a thing? Collaborating, or in the criminal sense, conspiring, for the sole purpose of crafting a new standard would trigger the need to manufacture an ‘enhanced’ product to meet a newly created standard. Manufacturers or members of the supply chain for a particular product would financially gain from such a plan. Who gets taken advantage of? The property owner and, by virtue of an increased sale price to cover expenses, potentially the buyer of a parcel.

Major Takeaways of Amendments To Existing Law

There are several major additions to bill (SB 124) that could become law in 2021.

- Two pool safety feature options must be in place. (AMENDED)

- Home inspectors must disclose the existence of a residential pool and list safety features. (NEW language)

- Pool safety feature options have amendments to their criteria and now incorporate ASTM Standards for pool safety feature options (ASTM F2286) and pool coverings (ASTM F1346) that could become problematic for property owners to maintain compliance. (AMENDED)

- Before a home or “parcel” can be sold by a property owner, there must be compliance with Chapter 515, Florida Statutes. (NEW language)

- The bill (SB 124) removes criminal penalties and replaces them with a noncriminal violation punishable as provided by s. 775.083, keeping the $500 fine. As with the current law, the waiver of the penalty is possible so long as the pool safety options are in place within 45 days of the issuance of a violation notice. (AMENDED)

- If signed into law by Florida’s Governor, it would take effect on October 1, 2021.

Conclusion

The goal of this bill (SB 124) is to prevent another tragedy. A good and noble action to undertake by Senator Hooper. The end result of instituting the additional requirement for a pool safety feature option would be to seek redundancy of safety measures. The idea being that where one safety precaution fails, another will prevent injury or death. In Kacen Howard’s case, the pool had a fence around it, but failed to prevent access to the pool and him drowning.

In my opinion, the requirement of simply adding another pool safety feature option was adequate to achieve the primary goal of preserving life. However, crafting additional criteria for almost every pool safety feature option was not necessary. As discussed, the incorporation of ASTM Standards into law could very well be problematic as there is no control as to when, or to what degree, ASTM Standards will change from one year to the next. As written, the legislation would require a property owner to now keep up with ASTM Standards in order to be in compliance with Chapter 515, Florida Statutes.

At the very least, legislators should place restrictive language, simply by adding the year of the ASTM Standard, to prevent the constant compliance dilemma when future ASTM F2286 (pool design) and ASTM F1346 (pool covers) Standards come out.

Stay Connected

Are you a licensed real estate broker or sales associate, a potential seller, or a potential buyer, a home inspector? I would like to know how you feel about this proposed legislation. Living out of state? If passed, this legislation could become a model for other states to enact in the near future. How would you feel if your state enacted the same legislative language?

Legal Disclaimer

This article was written for informational purposes only and should not be considered legal advice. Consult an attorney should you have any questions about this proposed law or any current law or regulation.

Florida Department of Health

Consumer Product Safety Commission

Please visit the Tips & Tricks Zone for more blog articles like this one. One of my most viewed blog articles is Polybutylene Plumbing Crisis – 99% Bad.

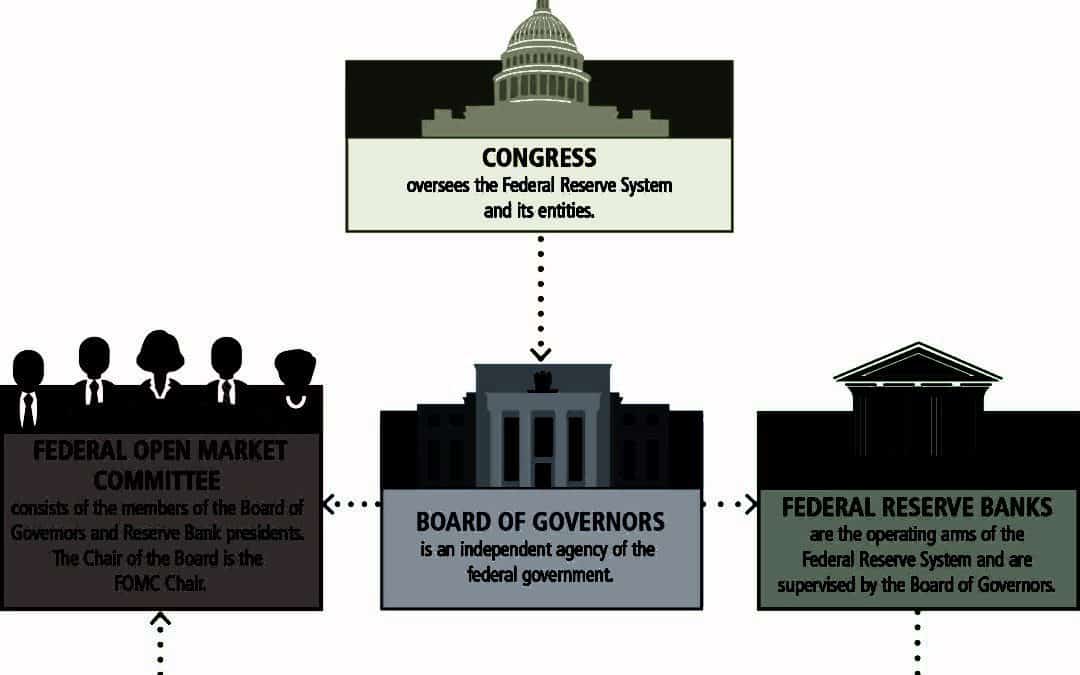

on March 19, 2019 and March 20, 2019. The FOMC will provide a “Summary of Economic Projections” report at this meeting and projections in the report may be the deciding factor on whether or not to raise the Federal Funds Target Rate (FFTR), which will in turn, trigger a rise in interest rate offerings by financial institutions. The report considers projections for GDP growth, the unemployment rate, inflation, and the appropriate policy interest rate.

on March 19, 2019 and March 20, 2019. The FOMC will provide a “Summary of Economic Projections” report at this meeting and projections in the report may be the deciding factor on whether or not to raise the Federal Funds Target Rate (FFTR), which will in turn, trigger a rise in interest rate offerings by financial institutions. The report considers projections for GDP growth, the unemployment rate, inflation, and the appropriate policy interest rate.

Recent Comments